Not sure which expenses are deductible in your tax calculation?

Can these costs be written off: fuel, internet, equipment?

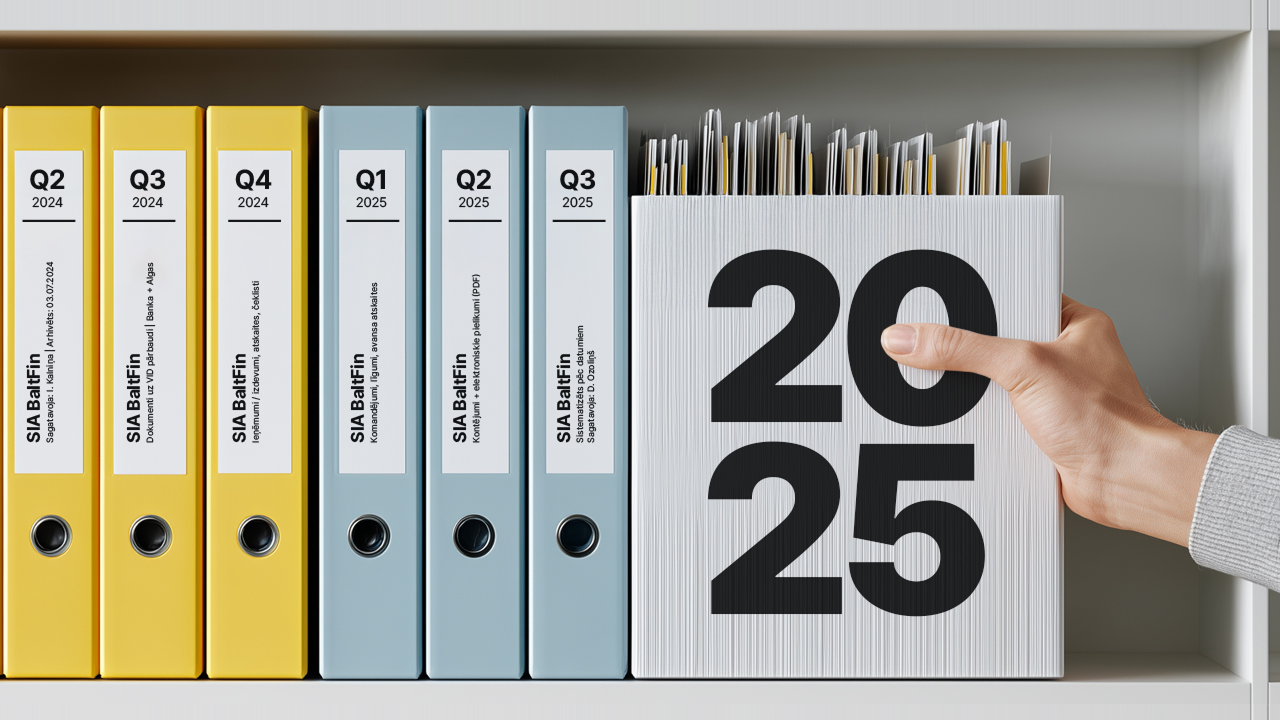

Automated accounting and tax calculation

Automatic reports, convenient accounting of income and expenses

Issue invoices, take pictures of receipts, synchronize bank account

Keep track of taxes, record income and expenses, submit reports, and receive timely reminders.

Automatic preparation of tax returns (VAT, CIT) and financial reports (Annual report, Balance sheet, P&L). Enter transactions, get automatically prepared reports.

From beauty professionals, couriers, designers to farmers.

Calculate salaries, enter overtime, sick leaves and vacations – everything is simple and transparent.

You just need to enter your data – income, expenses, receipts or invoices, and the system will calculate, sort and remind you of the rest.

Can these costs be written off: fuel, internet, equipment?

The system will advise you on which expenses can be deducted and in what amount. More expenses - less tax.

The system will automatically calculate net pay and all taxes, as well as prepare all reports.

The platform sends reminders and automatically prepares VAT, quarterly reports, and payroll calculations.

Bought a computer, but don't know how to write it off?

Depreciation is calculated automatically according to the selected method - in accordance with SRS requirements.

Choose an invoice design, add your logo, and send it. It looks professional and convincing.

Choose how to send the invoice: via email, WhatsApp or as a QR code. Fast, convenient and without unnecessary effort on your part.

VAT, PIT and social contributions in one place. Compare periods and follow changes in taxes in a single view.

Income, expenses and profit - visibly presented.

All transactions under control - much more convenient to keep records. Less manual work!

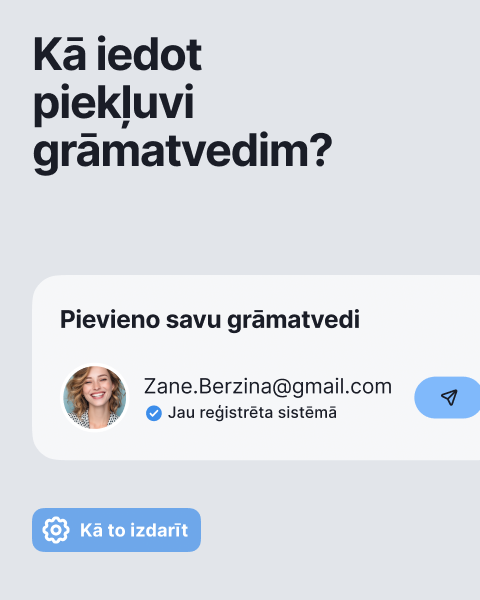

The accountant sees transactions, account statements. No need to search for files, no unnecessary communication - everything is transparent.

Forget about the calculator. Calculate salaries, hours worked and vacations automatically.

Reminders about deadlines. Mark as completed or add to calendar - everything is under control.

Invoices, tax calculations, reminders – everything happens automatically. No more Excel or manual work.

See how much you earn and where you spend. Use recommendations based on data of similar users to write off expenses correctly and safely.

VAT, quarterly and other reports are prepared automatically and are available for submission at the required time.

Invoices with payment status – see what has been paid, what is overdue and where to take action. No mistakes. No uncertainty.